Originally appeared at ZeroHedge

The events of the last several weeks have ominously demonstrated that dollar shortage has returned with a vengeance, as new headaches for virus-battered emerging markets will find it hard to cope with falling local currencies and demand.

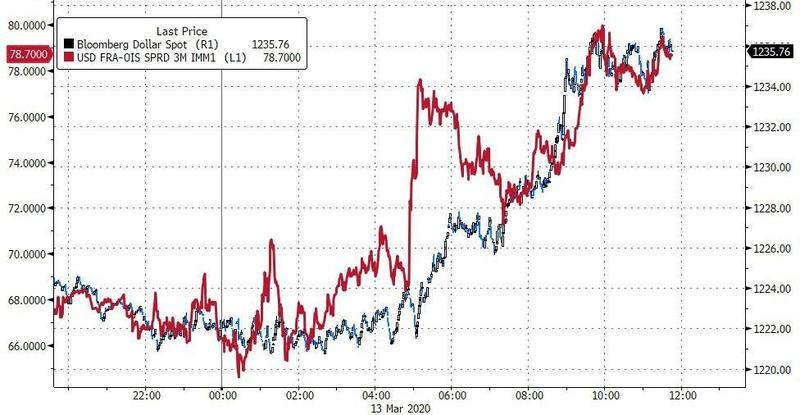

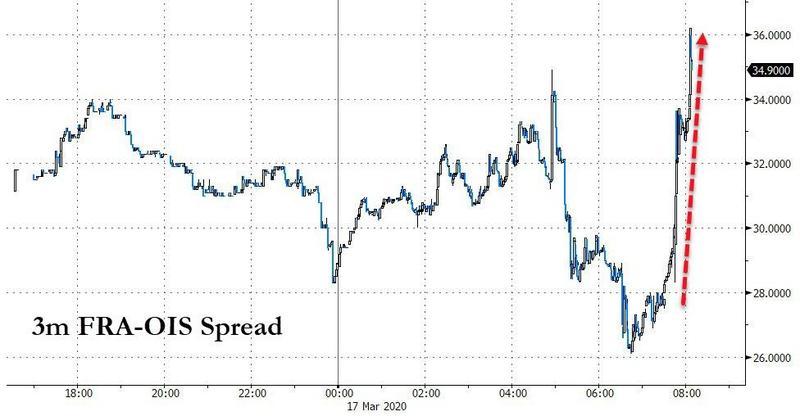

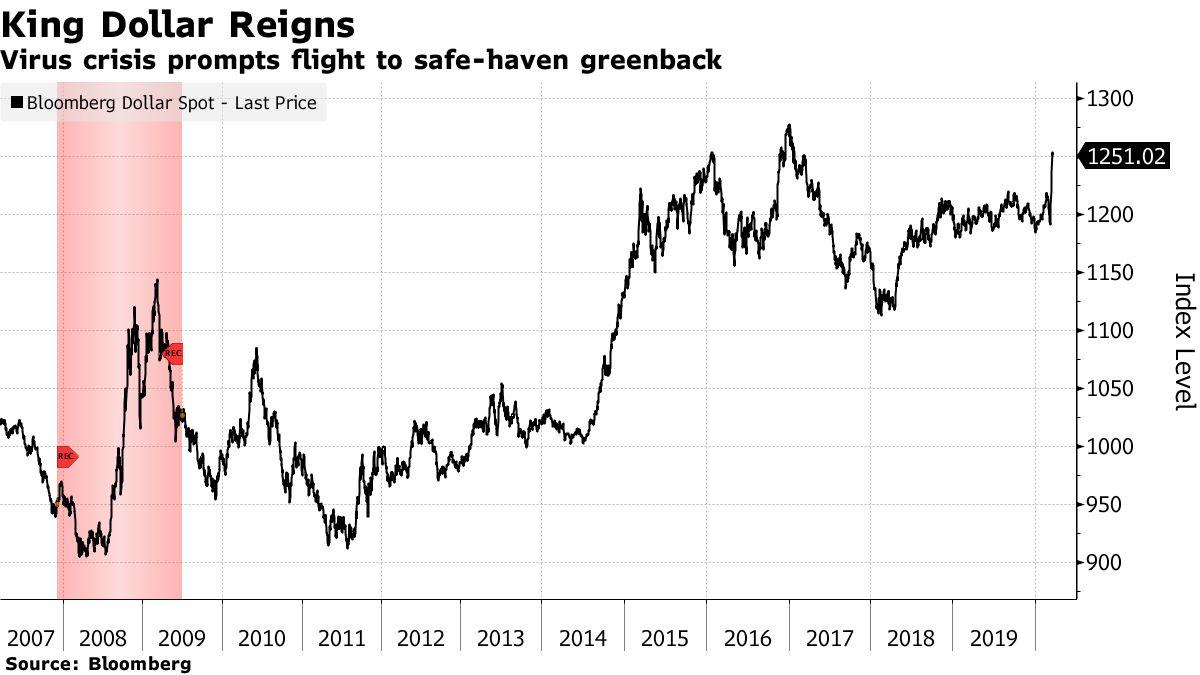

The dollar shortage was confirmed last week in both the Bloomberg Dollar index and the FRA/OIS spread, a closely followed indicator of interbank dollar funding availability that has spiked higher, indicating rising stress.

The Federal Reserve’s massive monetary “bazooka” including trillions of dollars for repo markets and the launch of $700 billion QE5 and return to ZIRP, as well as an emergency six POMO operations last week has failed to boost risk sentiment, and the FRA/OIS has yet to show any signs of relief, as it has surged to the highest level since the financial crisis.

The Fed’s monetary cannon may have solved the corporate liquidity crisis for the time being. Still, the dollar/liquidity shortage in the global financial system continues to worsen as investors are dumping emerging markets in record numbers and scrambling for dollars.

Marrying the supply chain disruption triggered by the Covid-19 crisis in China with the oil price war, this has crippled the petrodollar exchange system by sending the price of oil sharply lower and exacerbating the global dollar funding shock.

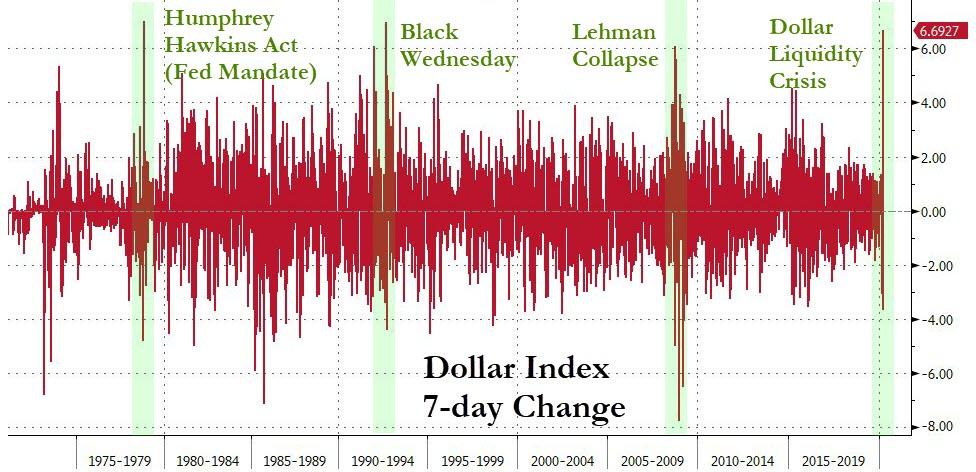

We’ve pointed out, the world is facing an unprecedented dollar margin call, as a result of the $12 trillion synthetic dollar short, some 60% of US GDP. With the dollar rising, the cost of servicing dollar debt for businesses and governments becomes more expensive as their local currencies plunge amid the barrage of rate cuts by global central banks.

“The surge in the dollar is another blow to emerging markets,” said Mitul Kotecha, senior emerging markets strategist at TD Securities in Singapore.

“The demand for the dollar has outweighed any hit to the US currency from sharply lower Fed rates. EM assets will continue to struggle as investors steer clear of relatively risky assets and maintain a bias for safe havens.”

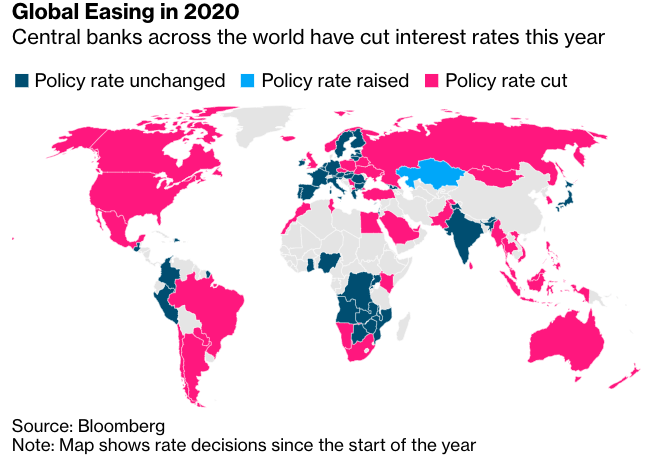

The Fed’s panic rate cuts on Sunday, welcoming the US back to ZIRP, has led to South Korea, Chile, Vietnam, Sri Lanka, Turkey, and Pakistan to cut rates as well. South Africa, Brazil, and Indonesia are expected to slash short-term interest rates later this week.

On top of dollar funding pressures, world trade growth is collapsing, and the tighter financial conditions on emerging markets have triggered a $30 billion outflow in 45 days since the virus crisis started, Bloomberg notes. The dollar reigns supreme in a crashing global economy and pandemic. For instance, the Mexican peso and Russian ruble have dropped by 20%.

Khoon Goh, the Singapore-based head of Asia research at Australia & New Zealand Banking Group Ltd., says emerging market economies are deploying rate cuts to cushion a hard landing but are using FX reserves for currency stabilization.

“They will continue to utilize their FX reserves to smooth currency volatility but will not seek to stem the trend or defend any particular levels,” said Goh.

“In the current environment, when external demand is very weak, allowing some currency weakness alongside lowering interest rates is the best way to try and ease overall financial conditions.”

The Australian dollar has tumbled to its weakest levels since 2003, a move that will increase import costs. Norway’s krone has fallen 15% this year, plunging to an all-time low as Brent tags the 27-handle this week.

Central bankers are making sure dollars continue to flow around the world. The Fed’s Sunday announcement called for reduced rates on its dollar-swap lines with five other central banks, a similar policy seen during the 2008 financial crisis.

“A strong dollar is typically a headwind for emerging-market currencies and even more so for countries that are reliant on offshore dollar funding and have floating exchange-rate regimes,” said Todd Schubert, head of fixed-income research at Bank of Singapore Ltd.

As the dollar shortage continues, tightening financial conditions in emerging markets, it’s only a matter of time before something breaks.

The best america can hope for is that when the sudden collapse does come, they land on top of the pile.

The petrodollar is dependent on saudi oil and the control of OPEC. It seems the saudis no longer want their oil price being dependent on a currency which is out of control.

So the US bombed their oil processing plant and blamed it on fuzzy wuzzy’s in the ME.

Good news for China…Dollar high means high production cost in USA and EU..so its better to invest in China and produce there!..

Ideal time to trade in other currencies for the trade of commodities and services between countries.

This resetting of global currencies has been long in coming, and one can stop a bit, throw panic aside, and look to financial movements of years since Trump took office,; makes one wonder if there was a not a bit of foreknowledge in play.

Bexit in Britain, Germany laying ultra conservative, many nations including Russia slashing its retiree pensions and slowing down of new social benefit programs, US military drawing down its forces and a exchange in Warfare proramming, and knocking back of huge costly weapons programs for increases in small less costly to build, cheaper to maintain by less high tech, and able to build in very large numbers that will increase firepower over what 1 multi millions jet aircraft can carry to site.

Domestic debt of conmers, in Federaly backedbloans, homes GI bills , student loans, home and auto, all with increasing defaults means the normal leveraging of loans 8x-10x was no longer sustainable; it was not interest as the collateral backer but the cost of processessing loan fees that boosted immediate short term accounts,.

The level of domestic debt of consumers and smaller ,under 10 million year range was into 15 trillion dollars, with over 40% not collectible but still in asset columns of paper holders.

Numbers of huge loans just to mergers places hundreds of millions out of circulation until mergers are complete, and today we see mergers in billions not millions being quite common.

The stock markets never were the true indicator of US Sovereign wealth and our Sovereign wealth is trillions in debt and barely able to continue paying just yearly interest.

It has not helped that the lowering of tax, royalties from mining timber and oil, placed nation into needing to borrow even more, and that income tax upon domesticly employed with over 49% paying 0$ tax, could not but return to treasury a little over 10% above cost of administering IRS itself.

Cuts put in place of social programs and cutbacks of equal pay for state cmnprojects are already set in place, causing more Metro and even State Bankruptcies.

Money to Israel and Egypt total higher than what some 5 states with more population recieve from Feds, and all in actuality comes from sale of interest bearing treasury notes.

The sale of say 500 million in Bonds leaves out the real cost to US of interest to be paid.

US Insurance of domestic overseas investments is running on a deficit , no actual cash on hand as its income goes into General funds, numbers on paper with no cash on hand, Social Security ring a bell.

Auto sales of domestic firms has never recovered since days of bailouts and even with company’s giving unions pension fund management and healthcare insurance programs partially paid by feds the firms are loosing ground.

If one looks at demographic seperation of the haves and have nots, it can be shown that the haves are primarily located in California, Texas and New England States, and it is that amount thrown into averaging that realy skews the totals to high side.

That small nations let themselves become so dependent upon US and Europes economies where does the blame lay, but in their own 1% gaining.

The recent photo op of Trump standing with 8 members of his cabinet showed a total personal worth of 47 billion dollars, and left out their connections to over 300 billions corporate cronies they came from and still are part of.

It is the poor in Europe and especialy those in British Crown dominions and US who will feel the future hammer blows, because Finance trumps, no pun intended, life.

What’s wrong with Kazakhstan?